The first two columns will show the period for which the lease activity is recorded by Date in (YYYY-MM) format, and the “Month” count.

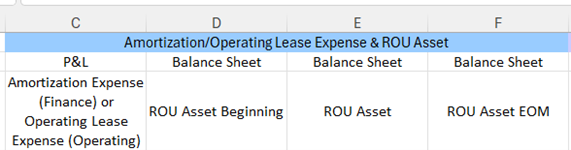

P&L Amortization Expense -Finance/ Operating Lease Expense- Operating (Column C):

Under ASC 842, operating lease expenses are recognized on a straight-line basis, while finance leases amortize the ROU Asset.

In the final month, the remaining amount ensures the ROU Asset value is reduced to $0.

ROU Asset Beginning (Column D):

Includes:

ROU Asset (Column E):

The reduction in the ROU asset.

ROU Asset EOM (Column F):

Total of the ROU Asset at the end of the month, incorporating Amortization.

LT Liability Beginning (Column G):

Interest Expense (Column H - Finance Leases):

LT Liability (Interest) (Column I):

Monthly accrual of total lease payment's interest portion.

LT Liability (Payment at BOM) (Column J):

Monthly payments processed at the beginning of the month (1st - 15th) that were included in the calculation of the lease liability.

LT Liability (Payment at EOM) (Column K):

Monthly payments processed at the end of the month (16th - EoM) that were included in the calculation of the lease liability.

Total ST & LT Liability (Column L):

The total remaining Lease Liability at the end of the month.

Long-Term Liabilities (Column M):

The portion of Long-Term Liability maturing within the next 12 months, per the standard that will be reclassified as current liability.

Short-Term Liabilities (Column N)

Current liability maturing within the next 12 months.

Long-Term Liabilities EOM (Column O):

Accumulated total of LT Lease Liability minus the reclassified ST Lease Liability as of the EOM.

Short-Term Liabilities EOM (Column P)

Accumulated total of ST Lease Liability as of the EOM.

Cash/AP for Lease Payment at BOM (Column Q)

Cash/AP for Lease Payments at EOM (Column R)

Cash/AP for Variable Lease Expense Payment (Column S) & Cash/AP for Non-Lease Payment (Column T):

Cash/AP (Summary of all Cash/AP Entries) (Column U):

Variable and Non-Lease Payments (Column V to X):

Specific entries made for variable expenses and non-lease costs are reflected in dedicated GL accounts.