The first two columns will show the period for which the lease activity is recorded by Date in (YYYY-MM) format, and the “Month” count.

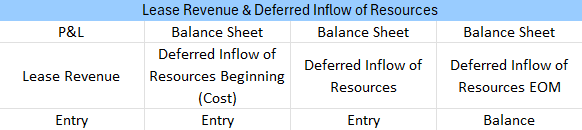

Lease Revenue (Column C):

Calculated by using the Deferred Inflow of Resources Beginning (Cost) divided by the Term.

Deferred Inflow of Resources Beginning (Cost) (Column D):

Reflects the sum of:

Deferred Inflow of Resources (Column E):

Shows the Opposite of Lease Revenue.

Deferred Inflow of Resources EOM (Column F):

Reflects the Total of Deferred Inflow of Resources at EOM.

LT Lease Receivable Beginning (Column G):

The PV of each Receipt back to the Start Date. Calculated as:

Receipt / ((1+discount rate/12)^Months to Start Date).

Interest Revenue (Column H):

The monthly Interest on the Lease Receivable. Calculated as:Discount rate / 12* Prior Month's End of Month LT & ST Receivable (less Beginning of Month receipts).

Note: Last Receipt of Lease is estimated to ensure Receivable is $0.

Interest Receivable (Column I):

Opposite value from Interest Revenue (Column H) less Interest Received as Cash. All Cash Received first goes towards Interest Receivable and then goes to reduce the Lease Receivable.

Interest Receivable EOM (Column J):

Reflects the Total Receivable at the end of month.

LT Lease Receivable (Receipt at BOM) (Column K):

Receipts from 1st - 15th of a Month will reduce Lease Receivable to an extent not used towards Interest Receivable.

LT Lease Receivable (Receipt at EOM) (Column L):

Receipts from 16th - 31st of a Month will reduce Lease Receivable to an extent not used towards Interest Receivable.

Total ST & LT Lease Receivable EOM (Column M):

Takes the sum of Lease Receivable entries for the Month.

LT Lease Receivable (Column N):

Amount removed from Long term Receivables for Lease Receivable that are within the 12 months as of current month.

ST Lease Receivable (Column O):

Amount reclassified for Lease Receivable that are within the 12 months as of current month.

LT Lease Receivable EOM (Column P):

Total balance of all Lease Receivable Entries minus Short Term Lease Receivable Entry (Column O).

ST Lease Receivable EOM (Column Q):

Running balance of all Short Term Lease Receivable entries. Calculated by using Last month balance + Column O).

Cash/AP for Lease Receipts at BOM (Column R):

Receipts collected between the 1st – 15th of the month.

Cash/AP for Lease Receipts at EOM (Column S):

Receipts collected between 16th – end of the month.

Cash/AP for Variable Lease Expense Payment (Column T) & Cash/AP for Non-Lease Payment (Column U):

Payments made in the month for Variable and Non-lease expenses.

Cash/AP (Summary of all Cash/AR Entries) (Column V):

Reflects the sum of Cash entries for the month.

Other Entries (Column W to Y):

Specific entries made for Variable Revenue and Other Income are reflected in dedicated GL accounts.